If you’re reading this newsletter, you read the trades. You subscribe to multiple other newsletters. So when Scarlett Johanson sued Disney last week, every Rich, Matt and Luke (the entertainment journalist equivalents to Tom, Dick and Harry) provided the simple explanation:

The big studios are prioritizing stock price over film profitability, and talent is mad.

That sentence is 100% true. But there is more to the story. Enough so that I think that requires a slightly deeper explanation of the forces at play. An “entertainment explained” analysis that really only I provide.

(By the way, with my new website redesign, I have an article linking to every “explainer” I have written. Check it out!)

Most Important Story of the Week - Wall Street Values Future Growth over Current Profits, Which Causes All The Problems

To summarize the ScarJo-Disney kerfuffle in five words:

“You can’t split the ‘g”’.

But what is “g”? And how does this tie to everything from ratings to box office to early Hollywood? Let’s explain.

The Curse of the Mogul - Talent Demands the Profits

One of my favorite theories for entertainment is the “Curse of the Mogul”. (Fellow strategy analyst Andrew Rosen brought it to my attention and references it fairly frequently.) To summarize, in any industry, there is a battle to “extract the profits” of delivering some good or service. Take the meat industry, for example. Farmers try to sell their cows for the highest profit. But since there are hundreds of farms, but only a handful of monopolized meat packing plants (that in the past have used illegal price fixing), the meat packers can extract the most profit.

In Hollywood, the “value chain” looks like this:

If you polled most people, and said, “Who deserves the most money in this value chain?” The answer would be talent. Because honestly, besides paying for the films and marketing them, do value do development execs and studio heads actually add?

But who actually takes the biggest cut? Probably the distributors--with local monopolies--and then the studios.

That’s a shame since talent is the most important part of the equation. I mean, they make the movies!

The curse of the mogul is that--when data is open and business models aren’t well-developed--talent can take a large share of the profits. Think about Robert Downey as Iron Man. He wasn’t just good as Iron Man; he became the character. You couldn’t make Captain America: Civil War or Avengers: Endgame without him. So he started demanding $50 million dollar paydays per film. And higher.

There are ways around the “curse” for studios. (Making IP/Brand more important than talent, for example) but they are tough to pull off. Of course, for talent to extract the profits, they need an open system with well understood business models.

The Old Days: Talent Demands Film Profits

In the olden days of, say, 2010, calculating a given film’s profitability was really easy. (Read my explanation here.) Since box office was highly correlated with future performance, and the business models were standardized, essentially by the Friday of a film’s opening, everyone from talent to the studio understood if a movie was profitable or not.

Let’s say that again: in the olden days, everyone agreed on whether or not a film was profitable or not. And they knew it quickly. And talent could share in that profit.

(The big caveat was “Hollywood Accounting”, which meant trying to use accounting tricks and gimmicks to steal money from talent. But that’s more unethical than clever strategy.)

I’d add, if a studio made a lot of profitable films, for the most part, they were rewarded with higher stock prices. Because more profit means a higher stock price. So talent, studios and Wall Street’s interests were aligned in making profitable films.

The New Days: Stock Price is Based on Future Growth

Nowadays, the studios all have streaming services. If those services do well, the stock price goes up. Hence, the focus is less on profitable films and more on stock price, as I mentioned above. But the “why” is key.

A warning: This is where we really board the train to “Wonkville”. I don’t want to make your eyes bleed with formulas, but I have to. I’m going to summarize an “Introduction to Finance” course in a few paragraphs. But if you understand this--and I’m banking on the fact that most of my readers (be they talent or journalists) who aren’t #FinTwit bros haven’t taken finance at all--you’ll have dived just a bit deeper than most.

So let’s start with this. The old school, book definition of the value of a stock is this:

The value of a stock is the sum of a company’s discounted future cash flows.

Technically, it’s the price of the total value of those cash flows divided by the number of shares a firm has issued. A stock is a piece of ownership, and what you own is the future money a company will make.

So let’s explain the two key pieces:

- Future Cash Flows: This is how much more (or less) cash a company has at the end of the year. Not profit mind you, since often firms manipulate that to pay the government less in taxes. Don’t worry about how to calculate this, just know that cash flows are all the extra money a firm has at the end of each year.

- Discounted: Since a dollar tomorrow is worth less than a dollar today, you “discount” or take a smaller percentage in the future. For example, if inflation is 2%, than a dollar next year is worth 98% of a dollar this year. In ten years time, if a firm will make a billion dollars, that’s worth say 81% in inflation-adjusted terms, or $810 million if you can save it.

Armed with this idea, stock analysts build models to predict future cash flows. Usually, they use current trends and inputs (like subscriber counts!) and then make five year or ten year “discounted cash flow” models. The analysts add up all the discounted cash flows, divide them by the number of shares outstanding, and they have their “price targets”.

Now, if everyone knew the future and could model discounted future cash flows perfectly, we’d have no need for a stock market. But predicting the future is hard! (Not for some Wall Street analysts who get quoted in trades and by CNBC. But it is true.) That’s why every different bank on Wall Street has a different estimate for different stocks. Most of the time, they herd around the same prices, but no two models are the same.

For example, if you take even the five year estimates of stock analysts for Netflix--the stock I always pick on--they all assumed Netflix would have had multiple years of free cash flow positivity by 2021. In fact, the consensus on Wall Street in 2016 was that Netflix would have $4 billion in Free Cash Flow this year!

In reality, they expect to just break even this year. Many models also had Netflix getting to 80+ million US subscribers by 2021, when it is at around 65 million right now. A prediction I got right!

See, predicting the future is hard!

(The Netflix stock, in fact, is an example of lots of analysts being “right” on the price, but for the wrong reasons.)

The Terminal Value and the “G”

But it gets even harder to predict the future the farther out you go. It doesn’t make sense to keep building a spreadsheet model with tons of inputs when you get past five or ten years. Because you’re just guessing at that point.

But you still need some value for all those future cash flows after say year 11. What do you do?

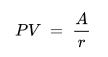

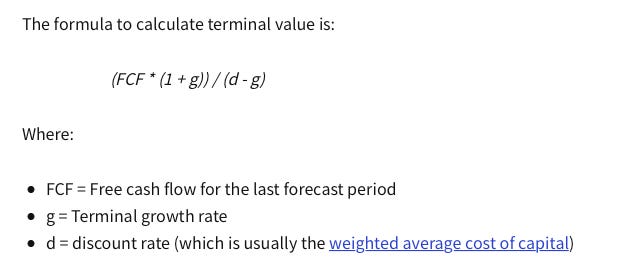

The solution is a “terminal value”, a concept I explained before. Essentially, the terminal value is a calculation of future cash flows. A “perpetuity” in finance terms, meaning a future stream of income that never ends.. The formula looks like this:

For a stock, we need to tweak that formula. The standard is to take the last “free cash flow” rate and add a growth rate. Which gets you this:

Essentially, you take the “discount rate” (the d) and subtract the “g”, which is future growth. That’s the “g” I’ve been talking about. It’s an assumption in a model about the future growth of an industry.

And it has HUGE impacts.

Basically, if the “g” goes up even a percentage point, a company can go from unprofitable to wildly profitable, just based on changing that one variable. Indeed, if you want to game a model, this is where you do it. Especially with the current generation of “unicorn” companies that have years and years of unprofitability in their forecasts. To justify their sky high valuations, at the end you just drastically increase the “g”.

And this has historical precedents. Even though Netflix has only achieved cash flow positivity once, in a pandemic-caveated year, its price was justified back in 2012-2015 based on having a high future “g”. Because the five year models often showed only negative free cash flow. So at the end, you make the “g” high, like past tech company’s growth, and boom, huge stock price targets.

The Specific Problem: You Can’t Split the “g”

The challenge right now is that Wall Street sees streaming as a high growth business. The “g” is premised on past tech stocks like Facebook, Google or Amazon.

At the same time, nobody is profitable. Meaning studios and streamers are losing cash each year in hopes of that future “g”. The high prices on streaming stocks (Netflix and Disney in particular) are predicated on lots and lots of future growth leading to sky high future profits. (Again, Netflix is profitable in an accounting sense, but not in a cash flow sense.)

And the incentives shift too. Disney, Warner Media and Netflix can make unprofitable decisions, but they will see their stock prices go higher. Again, because an analyst somewhere kicks up the “g”. (To be fair, growth rates aren’t the only way to boost a model, but it’s an easy one.)

Knowing this, using the “curse of the mogul” framework, talent could try to demand a split of future profits. And should. And that’s what Scarlett Johansen is doing. If ScarJo’s movie is being sold on Disney+ in expectation of future profits--meaning lose money now to make more later--she could demand more of that future money.

But, I mean, how? What will that future profit actually be?

That’s the key challenge: in the olden day, a film was immediately profitable. Even if the cash would flow in over a decade or more, everyone knew (within a margin of error) what it would be.

With future discounted cash flows for Netflix, Warner Media and Disney? No one knows.

Thus every proposed method to account for future growth has problems:

Say talent tried to tie their bonuses to stock price moves. Then every film released by Netflix--since Netflix is flat year over year--would be “unprofitable” for talent.

Say talent tried to tie their bonuses to subscriber growth. Allegedly Disney’s US growth is flat for the last few quarters, which implies that Black Widow didn’t help at all.

Say talent tried to demand a share of “attributed subscribers”. Well, if you read my multiple attempts to explain to calculate that, it turns out it is very, very low! (See my Great Irishman series for why I think Netflix lost money on that film.)

Say talent demanded shares of future profits. How do you agree on future profits when Wall Street analysts can’t even do that?

That last point in particular gets to the strangeness of the current situation. It would also mean that studios need to lose even more money now to pay for future profit. (Arguably, Netflix is doing this with large upfront payments to talent.)

Even worse: what if Wall Street changes their mind? What if they look at streaming and say, “Hey, it turns out no one makes money in streaming! We want profit, not growth at all cost.” If Wall Street changes its mind on the growth, a company loses money twice: the share price tanked and they already paid talent.

The Biggest Problem: Splitting a Smaller Pie

So that’s the challenge. You can’t share future profits very well, because they’re hard-to-impossible to slice up, yet Wall Street loves that potential for growth.

But there is a deeper issue, summed up by this quote in Matt Belloni’s newsletter:

“Thank you for calling out Disney’s misdirect here. Black Widow will end up the least profitable Marvel movie in years, no matter what they said in their press release.” — A finance executive

Essentially, in a streaming-only world of the future, the overall revenue pie for all producers and distributors is smaller than ever before. Using the “g” terminology, in a streaming only world, future “feature film” revenue may actually have a negative growth rate. That’s bad.

In that world, the production and marketing budgets for feature films just don’t make sense. And talent will take a haircut too. Everyone loses 35-50% in cash. And the “g” doesn’t help.

Almost Most Important Story of the Week - Delta Hurts Theaters and The “Decay is Real” for Streaming and Box Office

If it wasn’t for the Scarlett Johnansen lawsuit, the biggest story of the last few weeks has been the July “Covid Caveat” box office numbers. As of the first week of July, I would have called the box office numbers confusing, but now they are depressing again. Again, I’d stress that as long as the world is experiencing Covid, everything has a giant caveat next to it.

The current name of that caveat is Delta. With the current surge in cases, and mask mandates in some places, customers may again be avoiding theaters, even if they are fully vaccinated. In this uncertainty, we’ve seen one film decide to avoid theaters, Clifford the Big Red Dog.

That said, we’re still seeing films beat box office expectations. Though again, lowered expectations. Black Widow did set the record for the year, though much lower than past Marvel films. Space Jam 2 and The Jungle Cruise both beat their estimates, though only netting above $30 million each. We’ll see how long we’re in this lowered expectation phase and how long it lasts.

The other big wildcard is the impact of PVOD on these box office declines. Already, IMAX and theaters are blaming Disney’s dual-release strategy (and maybe Warner Bros) on fast decays at the box office. Do I buy this? Partly. I mean, if you give folks a view at home option, they’ll take it. And that could likely show up in the second weekend numbers.

But does it explain more than say Covid? Probably not. A single data point is not enough to draw a trend. So it’s an issue to monitor, but not proclaim a “new reality”. Yet.

Context Update - Biden Names Jonathan Kanter as DoJ Antitrust Chief

The latest news on the antitrust front is that President Biden appointed Jonathan Kanter as the head of antitrust enforcement at the DoJ. While not the strangest candidate, in recent years Kanter has become a foe of Big Tech, so consider this of a thread with Tim Wu at the Council of Economic Advisers and Lina Khan at the FTC. (And he’s much better than some initial alternatives, who had worked for Big Tech.) Even if it isn’t a guarantee that Big Tech is broken up, this isn’t good news for them either.

Other Contenders for Most Important Story

Space Jam as Franchise Builder

Over the weekend, I watched both Space Jam films with my daughter. (Or Space Jam and Internet Jam, as the sequel should be called.) As a kindergartner, she’s a bit unique because I showed her the new Looney Tunes originals on HBO Max when they first came on. She loved them. (Before that I had read her a little Golden Book called Bugs Bunny Marooned, which is what she calls it now)

So this begs the question: has any IP been more neglected than Looney Tunes these last two decades or so? Speaking with the kids of some of my friends, it is shocking that a generation grew up without knowing who Bugs Bunny is. That’s brand management malpractice.

So the WB franchise teams have a good opportunity here. They need to take a page from Disney and ensure they always have a good Looney Tunes on the air/stream, the way Disney always has a good Mickey Mouse show for preschoolers.

Dish and HBO Settle

The news that Dish finally settled with AT&T/Warner Media/HBO to return HBO channels to Dish service is fascinating from a “This story was still happening?” perspective. And it shows how much the shiny object in news coverage has shifted from linear stories to streaming ones. Reading through the tea leaves, I have to wonder if a change in corporate ownership helped get this deal across the line?