Does Hulu Make More Sense with Comcast or Disney?

The Most Important Story of the Week - 27 September 2022

Disney CEO Bob Chapek is everywhere lately, isn’t he? He did sit downs with THR, Variety and Deadline during D23, gave an interview to CNBC after that, and spoke at Goldman Sachs “Communacopia & Tech Conference”, an entertainment conference.

(I should say, “another” entertainment conference. By my count, there are twelve hundred such confabs each year.)

In each case, the headlines ended up circling around the fate of ESPN or Hulu. But that wasn’t all: just hours after Chapek pondered the fate of Hulu, Comcast CEO Brian Roberts, almost in real time at the same conference, responded, saying he’d be interested in bidding for it…if the price was right. Paramount Global CEO Bob Bakish said the same thing at the same conference.

Hulu, Hulu, Hulu!

Everyone seemingly wants to know what will happen to the country’s second biggest streamer. And frankly so do I. A few weeks a go, I wrote that, far from thinking it’s a no brainer, it actually might make sense for Comcast to buy Hulu. And you know I tend to be skeptical of M&A solving a company’s strategic issues.

Ponding the “Hulu Conundrum” more, I could make the case that both Disney and Comcast would be better off with it, and that they both might also be better off selling it!

The fate of Hulu is big enough that—even though we didn’t get any real new “news”—it’s the most important story of the week. I’m going to lay out what I think about Hulu’s advantages and disadvantages under both Disney and (potential) Comcast ownership.

Most Important Story of the Week - What is (and should be) the fate of Hulu?

I assume most of my audience knows about Comcast and Disney, and their various strengths and weaknesses as companies, but it’s worth repeating what Hulu, as a streamer, brings to the table.

I’d highlight these key facts:

Hulu is only distributed in the U.S. It has 42.4 million U.S. streaming on-demand subscribers. From those subscribers, according to Disney, Hulu makes $12.92 per subscriber per month.

Hulu also offers “live TV”, known in the biz as a “virtual” MVPD, which generates a whopping $87.92 per month from 4 million subscribers.

Based on those numbers, Hulu could make above $10 billion in revenue per year. We don’t know how much profit Hulu makes on that $10 billion, and so far Hulu has only been reported as profitable in Q3 of 2021.

By usage and some other metrics, Hulu ranks either second or third in the U.S. behind Netflix.

The backbone of Hulu’s content library is day-after-air TV from Fox and ABC. Since Disney owns ABC, that content will likely stay, but Hulu likely owes a license fee to Fox for this content. Meaning, at some point Fox could pull their content. (But I don’t know this for sure, as the actual legal contracts aren’t public.)

Owning the second biggest streamer in the U.S. is a valuable proposition. But how valuable? Whenever this comes up, I need a framework to organize my thoughts, so let’s trot out my favorite...

The 3C-STP-4Ps Framework

My favorite business “framework” is Harvard B-School’s 3C-STP-4Ps product marketing analysis. Originally designed for “consumer packaged goods”, it works great for streamers too.

(Why haven’t I written an article on this then? Good question! It’s on my writing to-do list.)

For today’s look, we’ll simply evaluate Hulu using the “4Ps”. To truly evaluate a strategy, we’d have to understand the 3Cs and the segmentation, targeting and positioning, but we don’t have time for that. I will tweak the 4Ps slightly, though. Traditionally, the 4Ps are: product, price, promotion, packaging and placement. (Yes, that’s 5. Welcome to framework creep.)

I modify these categories for the streaming services thusly:

Product: Content

Product: User experience/tech

Promotion: Marketing

Placement: Distribution

Price

In other words, I eliminated “packaging”, since it doesn’t really apply in a digital world. You could argue that “UX” is packaging, but I think that undersells the role of UX as a part of the product itself. UX isn’t simply how the app/streamer looks, but how it performs. Thus, a streamer’s product is a combination of both their content and the experience trying to get to that content.

If you want to know, I value those categories like this:

Content 50%

UX: 20%

Marketing: 20%

Distribution: 10%.

Read that as, “if you’re trying to attribute the success or failing of a streamer, 50% of it is due to content, 25% to the user experience…” and so on. One of the reasons I focus on content so much (and think the ratings matter for that content) is because it’s literally half of the streaming wars battle.

For this analysis, I should add one more number, the “financials”. In any M&A deal, price matters. Almost any company is a good value at the right price, and almost any deal is terrible if it costs too much.

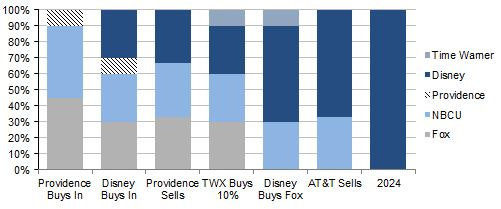

By finances, I mean the cost it will take to keep or acquire Hulu if you’re Disney or Comcast. As a reminder, Comcast owns 33% of Hulu right now, as this brilliant chart on Wikipedia shows:

Back in 2019, after Disney bought out then AT&T’s 10% stake in Hulu, they decided to buy out Comcast as well to achieve total control. The two companies agreed to pay Comcast for their 1/3rd control for a minimum price around $27 billion dollars. Meaning they have to pay Comcast about $9 billion in 2024.

So that’s the likely price Disney will pay Comcast, valuation-wise.

What’s the ceiling? Well, folks pointed me to this CNBC article where, incredibly, Comcast execs anonymously think Hulu is worth much, much more than that. Something like $50 billion, with it peaking at $60 billion during the pandemic. (Though this is honestly just bad economic thinking. Hulu was never worth $60 billion in 2021, but due to inflated valuations, folks would have paid that crazy number in 2020. But that has no bearing on current values! Those were inflated/unrealistic valuations!)

So what do I think Hulu is worth? Right now, almost exactly $27 billion.

Consider Netflix as a proxy. Since they are the only publicly-traded, streaming-only company. Right now, their “enterprise value” is about $100-110 billion all in. But they’re global, whereas Hulu is U.S. only. By revenue, the UCAN region is about 43% of Netflix’s total revenue last quarter. So let’s take out Canada and call it 40%. So that would mean if Hulu is the same size as Netflix, is worth say $40 billion. But it’s not! It’s 70% as big as Netflix by subscribers. (Less for ARPU, but go with it.) 70% of $40 billion is…$28 billion! Meaning yes, Hulu is likely worth what Disney and Comcast agreed to back in 2019.

The other factor to consider is that one of the main drivers of Hulu’s valuation—which presumably comes from the potential cash flow it can generate—is the subscribers it has and the money they can spend. Again, that’s about 42.4 million video-on-demand subscribers and another 4 million vMVPD subs, meaning if you buy Hulu, you’re buying those subscribers. Here’s that line:

To help understand this deal, I made a table. So let’s add our first three lines:

Content

Content is the most important of the “4Ps” for streaming, and looking honestly at what Hulu has, it’s not that impressive.

As I wrote for the Ankler this week, most of Hulu’s value comes from day-after-air television shows, and notably, as I wrote in the streaming ratings report this week, NOT their Originals. Until recently, they really didn’t have any huge hits on streaming. That’s not for a lack of trying, as they released a lot of shows, especially under their “FX on Hulu” label.

But this is a double-edged sword, and makes evaluating the fate of Hulu fairly tricky. If Disney sold Hulu to Comcast, does that includes “FX on Hulu” shows? Or licensed 20th Century Fox TV shows? And if those FX-on-Hulu shows do go with Hulu, how long is the licensing deal, since 20th Century Fox produced many of them? Would Comcast insist that ABC shows must stay on Hulu for say ten years, so that Disney can’t do to Hulu what Comcast just did? (They’d probably have to negotiate with Fox separately.)

I can’t stress this point enough: when I look at the content on Hulu, I don’t see a lot of value.

At least not valuable content that Hulu will be able to hold onto for the long-term. I’d sum it up as “some originals, a lot produced by 20th Century Fox, and potentially some day-after-air TV.” So let’s update our table with the content someone would either keep, or buy:

User Experience/Tech

Hulu brings a couple of things that are arguably more valuable than the content, given how little control Hulu has over their licensed content. First, they aren’t just a streamer/ad-supported streamer, they also have an “virtual MVPD”, meaning a Live TV service like cable. They currently have 4 million subscribers to YouTube TV’s 5 million.

In addition, they allow folks to add other subscriptions to their live TV service, like Starz and HBO Max. This is similar to Roku, Amazon and Apple TV’s “channel” services, where they sell subscriptions for a cut of the recurring revenue. They also bundle Disney+ and ESPN+ with Hulu Live TV.

It hasn’t all been smooth sailing—see regular crashes during high viewership live events like The Super Bowl or NBA Playoffs—but they have that capability. They also have one of the better ad-technology stacks in the streaming business. Those are two capabilities presumably Disney would like to keep.

Or do they? It’s been rumored that Disney valued the technology/capability it got when it bought BAMTech (formerly MLBam) more than Hulu. That’s why they used BAMTech to build out Disney+, rather than Hulu’s technology. So it’s complicated.

Comcast owns some similar technology already, too. They have Peacock up and running, and it already has advertising. And they own a FAST—free, ad-supported, streaming TV service—via Tubi, so they can offer linear channels. (Peacock has linear channels too.)

But they don’t have a virtual MVPD in-house. Meaning, Hulu’s technology has some value, but Comcast has a lot of those same capabilities.

Marketing

Yeah, this is a push. Hulu doesn’t bring any true marketing advantages to the table that Comcast and Disney don’t already have. (The best part of their marketing efforts that I could come up with was that their ads are kinda funny.)

(Disney is the clear number one at cross-company marketing, meaning the ability to leverage multiple parts of a company to drive a marketing campaign (from paid advertising to on-air promotion). Comcast is pretty clearly second, with Warner Bros. Discovery trying to catch up. Amazon and Apple obviously have their built in capabilities too, with Amazon being much stronger due to their homepage.)

Distribution

Hulu is distributed fairly widely, and probably pre-installed just slightly more on devices than Peacock, but not much. As for distribution, via various distributors like Roku, Amazon Fire devices and Apple, Hulu is basically second or third after Netflix and Prime Video. That’s a powerful distribution position, but distribution is only about 10% of the puzzle in my estimation.

But does it have that much more than Disney+ or Peacock? Maybe marginally more than Peacock.

Pricing

I laid out what Hulu charges earlier, but this is the section where it is worth pointing out the prevalence of the “Hulu bundle”. Part of Disney’s success has been aggressively pushing their bundle of Disney+, Hulu and ESPN+.Some non-trivial amount of customers subscribe to Hulu through the bundle, and ripping Hulu out of that wouldn’t be easy.

Of course, if Disney combines Hulu’s content into Disney+…that changes this whole analysis, doesn’t it?

Notably, when Disney launched Disney+ in the U.S., they had to launch a “bundle”, because Hulu was already a separate joint venture. However, when they launched Disney+ in India, they just launched included Disney+ in the existing “Hotstar” streamer they acquired from Fox. So it was an “all-in-one” streamer. They did something similar in the UK and other territories too.

Bob Chapek has more than hinted this is the ultimate fate of Disney+ in the U.S. too. But then this begs the question: what value does Hulu still have if Disney is going to basically shut it down anyways?

In my mind, this is the biggest reason why Disney could sell Comcast to Hulu eventually. If Hulu brings so little in terms of UX, marketing and distribution that you’d fold it into Disney+, then Disney would only need it for the content, and the only content you can’t fold into Disney+ is arguably Fox’s day-after-air TV. (A lot depends on what would be negotiated and what is legally contracted to Hulu. It’s complicated.)

So Add it Up…

Here’s my stark conclusions running through this analysis:

First, if I’m Disney, I would sincerely consider selling Hulu, especially if the price is high enough. There just isn’t that much valuable content that Hulu controls, in particular, for Disney to pass on a $50 billion valuation (if Comcast offers something that crazy).

Second, if I’m Comcast, I’d buy Hulu, but only if the price was low enough. Besides subscribers—which they do need—Hulu on its own doesn’t really bring that much. But given that it looks like they’re the odd man out of the streaming wars with Peacock, Hulu could revive their fortunes.

But a lot depends on the specifics. If Comcast can negotiate to keep ABC and Fox day-after-air TV, then Hulu becomes much more valuable.

Yes, a lot rides on the price, but that’s my take on most deals. (A point too often neglected by media coverage of M&A deals, in my opinion.)

And that’s why I could see Disney selling if Comcast really does offer a huge sum. Consider this: Comcast will try to go to an arbitrator and tell them they think Hulu is worth $50 billion dollars. Imagine if Disney says, “Fine, we’ll knock 40% off the price and let you pay us only $20 billion to own Hulu.” Then Comcast would look pretty silly if they had to say, “Uh, no, we think Hulu is worth $50 billion for Disney, but less than $30 billion for us.”

Of course, I like the deal even better for Disney if they can switch from spending $9 billion (likely in debt) and making some money on the deal. Disney’s debt worries me more than Comcast, since Comcast has much larger cash flow each year. (Though in EBITDA-to-net debt ratios, the two companies are fairly close.) Plus, depending what they negotiate, Disney wouldn’t really lose too much. ABC day-after-air shows could come to Disney+, and so could all the 20th Century Fox and FX shows eventually.

But then why would Comcast buy Hulu? I see three major reasons why after doing this analysis. First, Peacock is in seventh or eighth place in terms of paying U.S. subscribers. That’s bad. Buying Hulu immediately makes them a top tier player, however they combine it. And that ties to reason two, which is that Comcast LOVES to make deals. They just love it. Third, I think Comcast could really imagine a lot of value for Hulu Live TV. In some ways, that’s the next generation of the cable bundle, and Comcast knows cable. (Right now, Hulu Live TV makes almost as much for Hulu as streaming video-on-demand right now.)

So What Happens?

Eh. Who knows?

Not to be flippant but predicting M&A is one of those arenas where we don’t have a lot of data. Past deals sometimes owe more to luck than economic logic; Discovery bought Warner Bros. from AT&T because of a chance meeting. Other deals have happened simply because a CEO decides the deal will happen. If Comcast CEO Brian Roberts decides Comcast must have Hulu to compete it could happen and Disney likely would love to go from paying $9 billion to potentially getting paid tens of billions.

That said I’m sympathetic to the idea that all of this is posturing all around. Basically, Comcast wants to pretend Hulu is much more valuable than it is so they can get Disney to pay them more.

If I had to bet, I’d bet on the status quo. If nothing changes, Disney will someday pay Comcast $9 billion to control all of Hulu and do whatever they want with it. That feels like the likeliest outcome, because of simple inertia.